Understanding how mortgage escrow works and its requirements is the first thing you must do before figuring out how the process goes. Without a doubt, the entire process of purchasing a house is very complex and difficult. Moreover, if you do not understand or are unprepared, it seems generally impossible to carry out.

From procedures like getting your mortgage approved to home inspections and other possible processes that may happen. On the other hand, being in escrow is another complicated thing that you may find difficult. But you are on the right page because everything you need to know will be mentioned in this blog post.

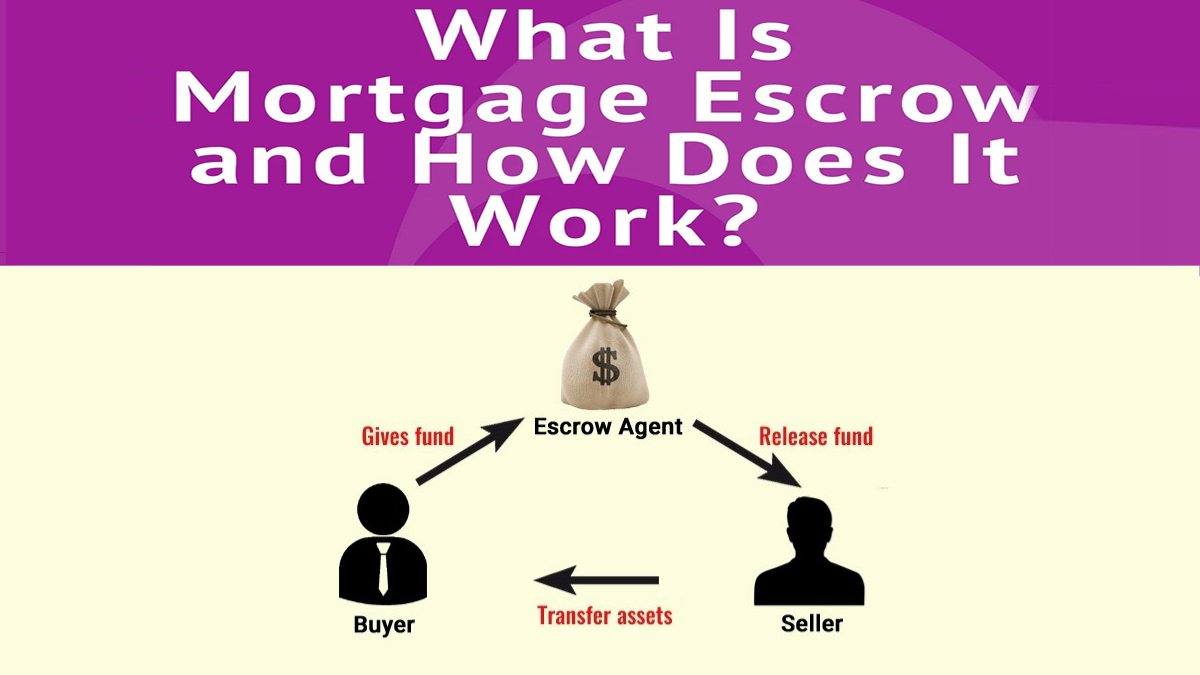

What is Mortgage Escrow?

A mortgage escrow is a type of account that is used to pay and collect insurance payments and property taxes on a home. This is mostly used by homeowners and mortgage lenders, and its purpose is to ensure that the taxes are paid and your property is insured. It also helps to decrease the risk of you defaulting on the loan repayment for banks.

A mortgage escrow is a special holding account for homeowners where funds are kept and managed until the contract is fulfilled and completed by a third party. Generally, escrow is known as a financial instrument and an account managed by a neutral third party as an agent for two parties in an agreement or deal.

How Does Mortgage Escrow Work?

When it comes to mortgages, here is how escrow accounts work. So, the escrow account is used to guarantee that the homeowners’ insurance premium is paid on time as well as property taxes. Moreover, you are required to pay less than 20% on all government-backed mortgages and conventional loans.

With this in mind, when you have a mortgage escrow account, you get to balance and maintain payments for your bills. In addition, you get notified if there are changes in your account’s balance, and every year, your account will be audited.

Mortgage lenders gather enough funds to cover the cost of your insurance and taxes for the next year and will divide it by 12, then it will be added to your monthly mortgage payment.

When Do You Need an Account?

You need a mortgage escrow account if you are financing your home purchase with a USDA loan or FHA loan. You also need this type of account if your down payment is less than 20%. What’s more, in some parts of the country, this account type is known as an impound account and is required by mortgage lenders.

Who Controls an Escrow Account?

Who controls the escrow account? This is one of the frequent questions a lot of people ask and need answers to. So, if you are interested in finding out, here is what there is to know. Firstly, sellers and buyers make use of a bank or title company to act as an agent that will be responsible for the management of the money deposit during the process of home-buying.

So, if you eventually become a homeowner, the mortgage lender is going to be in control of the escrow account. What’s more, the lender will transfer a part of your mortgage payments to the mortgage escrow to cover taxes and insurance. However, there is no set rule or instruction that says that the lender must be in charge and control of the escrow account.

Pros and Cons of a Mortgage Escrow Account

Here are the pros and cons of a mortgage escrow account:

Pros

- Safeguard you from tax liens.

- Possible lower mortgage costs.

- When there is a shortfall, you are covered.

- Removes two bills from your debt list.

- Secures your down payment.

- It is automatic.

- Insurance and taxes are covered.

Cons

- Interest is not normally earned.

- Large upfront deposit.

- You are not in control of your money.

- Monthly mortgage payments can fluctuate.

- You may miss investment opportunities.

- Prone to scams and fraud.

- Possible inaccurate estimates.

Even though there are benefits and advantages to using this type of account, there are also some downsides that you can’t run from. This is why it is important that you prepare yourself before taking the next step.

How to Set Up a Mortgage Escrow Account

If you would like to set up a mortgage escrow account and begin your home purchase process, as someone interested in buying a house, your broker will send your down payment into the escrow account and release it when the time is right. This means that you do not have to create an account by yourself or even make deposits. In addition to this, you can even open this account in person, by phone, email, or phone call.

So, here is what you need to do:

- Get in touch with your mortgage provider.

- Gather and provide all the important documents and information.

- Read and sign the paperwork.

- Make your down payment.

- Make ongoing payments.

Once you finish making payments, you can go ahead and close the escrow account. However, remember that the closing process varies.

Leave a Reply