In today’s world, there are several loan platforms and loans available for whatever need you are applying for. A credit-builder loan is a method that helps you build credit as you make payments towards your loan. Are you here in search of what a credit-builder loan simply talks about? Then you are in the right place; this article will provide you with all the necessary information about it.

What is a Credit-Builder loan?

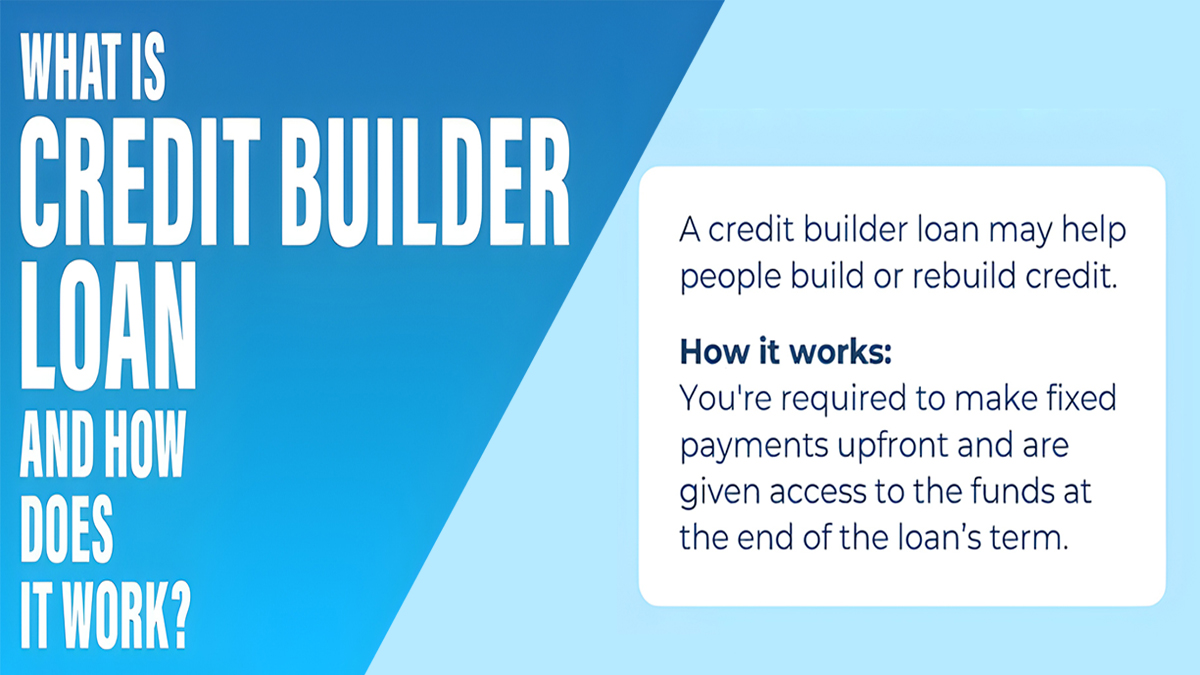

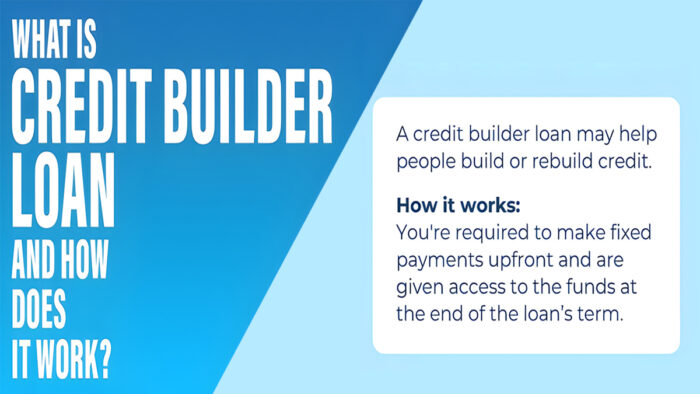

A credit-builder loan is a financial tool designed to help individuals establish or improve their credit history. Essentially, it’s a type of loan where the borrowed amount is typically held in a savings account or certificate of deposit (CD) as collateral. The borrower then makes regular payments, and once the loan is fully repaid, they receive the initial borrowed amount plus any interest earned.

The key feature is that the lender reports the borrower’s payment history to credit bureaus, helping them build a positive credit history over time. It’s a useful option for those with limited or poor credit, as successful management of the Credit Builder Loan can contribute to an improved credit score.

How Do Credit-Builder Loans Work?

The normal loan process, as we all know, comes with a wide range of loan amounts and their means of repayment. A credit builder loan allows you to lock your money in your savings account until your interest is met before it is disbursed to you.

Whether you’re rebuilding your credits or building first-time credits, considering a credit-builder loan is advisable. This loan differs from every other type of loan that we know of in our world today. Having a credit builder loan allows the lender to put aside a certain amount of his or her money in an account for saving, and a payment is made towards the account in monthly installments. At the end of the term of the loan, the lender receives the balance.

A traditional loan works the opposite with credit-building loans. Traditional personal loans come with a wide range of repayment terms and amounts. For a traditional loan, as we know, a lender will release a certain amount a borrower is qualified to receive. 30 days after the loan is given, the borrower pays it back in monthly installments, including interest. While credit-building loans allow a lender to place your loan in a savings account you can’t have access to, your funds are only available after your monthly payments.

How Much is a Credit-Builder Loan?

The amount of the credit-builder loan depends on the interest rate. Not all lenders have the same interest rate; the rates and fees of lenders vary. Just note that the higher the borrower’s interest rate, the higher the monthly payments and total cost may be.

How to Get a Credit-Builder Loan

Searching and shopping around and not just sticking to one can help you find the most affordable loan option that works for you. So if you want to get a credit-builder loan, then just follow these steps below;

• Link with Lenders That Offer Credit-Builder Loans

Make research on lenders that offer capital-builder loans. Not all lenders render the service of a credit-builder loan plan.

• Decide on the Amount You Want To Borrow

When you eventually search and pick a lender you want to borrow from, it is also important to know the amount of money to borrow for the expenses you want to cover. Determine how much you can easily commit to your credit loan account.

• Browse for the Best Term

Browsing around for the best term requires you to shop around for the lender’s policies and their method of administration. Some lenders collect a late payment fee and other terms. Get more information about their services and know if they favor you.

• Tender a Formal Application

Lender requirements vary when it comes to what is needed for formal applications, like contact information, proof of income, identification numbers, and names. So once you have finally decided on the lender to work with, take enough time to familiarize yourself with their loan application process and endeavor to collect all the necessary documents you’ll need.

• Proceed to Payment

First of all, after the approval of the credit-builder loan, it is important to know the payment mode to be submitted. Make sure to know when the payment is due, and it is necessary to make your payment timely according to the agreement with the terms and conditions.

Where to Get a Credit-builder Loan

Getting a credit-builder loan really doesn’t take much searching; the loans are available at some of the same institutions that offer traditional loans, and here are the following places to get them:

- Credit union

- Lending individuals

- Local community banks

- Online Lenders

Note: Always compare terms, interest rates, and fees to make an informed decision. If you’re unsure, a visit to your local bank or credit union would be a great place to start!

How to Manage a Credit-builder Loan

Whether you have a credit account or are just borrowing for the first time, here are some steps you can follow to enable you to manage your credit-builder loan effectively:

- Learn to gauge your budget before deciding to take any form of loan.

- It is necessary to check the features of different credit-building loans so you can compare offers. The more you compare, the more likely you are to see the ones with the best deal.

- Another way you can manage your credit-builder loan is by making your payment on or before the agreed-upon date.

- Set up a credit monitoring service for your credit-builder loan as you pay off the loan. This will enable you to keep in touch with your payments.

Remember, building credit takes time, so be patient and stay disciplined in managing your credit-builder loan.

Advantages of Credit-builder Loans

Getting a credit-builder loan has advantages you can enjoy, which include:

- It’s highly accessible. You can get it online or from any commercial bank around.

- It helps you generate payments to increase your credit score, especially when you have no record of borrowing history.

- A credit-builder loan offers lower interest rates. Unlike the normal traditional loan, where on every amount you tend to borrow, there’s always interest to be paid for borrowing.

Obtaining a credit-builder loan is very accessible, and it can be done online or by visiting a nearby commercial bank. The advantages of obtaining a credit-builder loan are listed above.

Disadvantages of Credit-Builder Loans

Before you decide to get a credit-builder loan, it’s advisable to be familiar with not just the advantages but also the disadvantages involved, which include:

- Payments are made before funds are available to you for use.

- It’s another debt that you need to pay back. Every loan has an interest rate, though the credit-builder loan has a considerable interest rate.

- Missing a payment can be risky. Every payment made tends to gather and accumulate in your account to help you meet your target.

- It doesn’t allow the free flow of funds to you. It can tie up your funds to a place for some period of time.

Reviewing the cons known as disadvantages before jumping into the offer is very necessary to avoid any sort of bridging the contract when finally realized.

FAQs

Can I be Denied a Credit-builder Loan?

Yes. A credit-builder loan can be denied if you do not meet the requirements. Credit-builder loans are sometimes issued alongside your requirement to know if you are eligible for the loan.

How Much Can My Creditor Loan Me?

The amount the lender can loan you depends on your qualifications and whether you once had a credit account. They ask for what you will be using it for and what you have currently.

What Happens If I Skip My Payment Day?

Your credit score will likely drop if you skip your payment day. Evaluating and recording your payment days can help you put a great hedge against knowing when to pay into your credit-builder account.

Leave a Reply